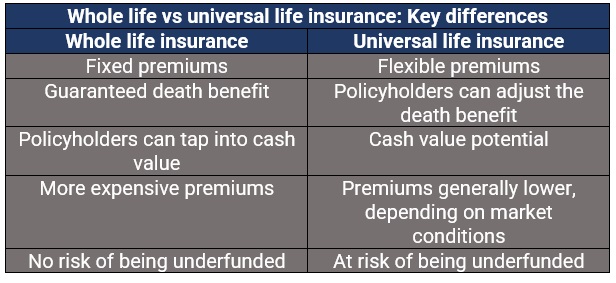

Understanding Whole Life Insurance: Key Benefits for Your Financial Future

Whole life insurance is a type of permanent life insurance that provides coverage for the insured's entire lifetime, as long as premiums are paid. One of the main benefits of whole life insurance is its ability to build cash value over time. This cash value accumulates on a tax-deferred basis, making it an attractive option for individuals looking to enhance their financial planning strategies. According to Investopedia, the policyholder can borrow against the cash value or even surrender the policy for its cash value if needed.

In addition to the cash value component, whole life insurance offers a death benefit that provides financial security to your beneficiaries upon your passing. This can be a vital part of your estate planning, ensuring that loved ones are not burdened with debts or expenses. Another key advantage is the predictability of premiums that do not increase with age, allowing for better budgeting of your long-term financial commitments. For further insights on whole life insurance and its benefits, visit NerdWallet.

Is Whole Life Insurance the Right Choice for You? Evaluating Your Options

When considering whole life insurance, it's crucial to evaluate whether it aligns with your financial goals. Whole life insurance provides lifelong coverage and includes a cash value component, which grows over time. However, the premiums can be significantly higher than term life insurance. Assess your budget and long-term objectives to determine if the benefits outweigh the costs. If you're looking for lifelong coverage without the worry of expiration, this option might be worth exploring. For a comprehensive look at whole life insurance versus term insurance, you can check out this Investopedia article.

Before making a decision, it's essential to consider your personal circumstances and financial situation. Whole life insurance can be an excellent option for those who want to build cash value and leave a legacy. However, if you're primarily seeking affordable coverage for a specific period, term life insurance might be more suitable. To better understand your options and make an informed decision, consider consulting with a financial advisor. For more insights on choosing the right type of insurance, visit Forbes.

How Whole Life Insurance Can Serve as a Foundation for Wealth Building

Whole life insurance is not just a safety net for loved ones; it can also serve as a powerful tool for wealth building. This type of permanent life insurance provides a guaranteed death benefit, which can be an essential part of a comprehensive financial plan. Additionally, whole life policies accumulate cash value over time, which grows at a predictable rate. By contributing to the cash value component, policyholders can create a source of funds that can be accessed through loans or withdrawals, making it an appealing option for those looking to supplement their retirement income or invest in other ventures. For more insights on how whole life insurance can build wealth, visit Investopedia.

Furthermore, utilizing whole life insurance as a foundation for wealth building offers tax advantages that can significantly enhance an individual’s financial strategy. The cash value growth is tax-deferred, meaning that policyholders won't owe taxes on the growth until they withdraw funds. Additionally, the death benefit is typically received by beneficiaries tax-free, allowing for more efficient wealth transfer. This dual functionality makes whole life insurance a unique financial instrument. To explore more about the benefits of whole life insurance, check out the resources on Forbes.